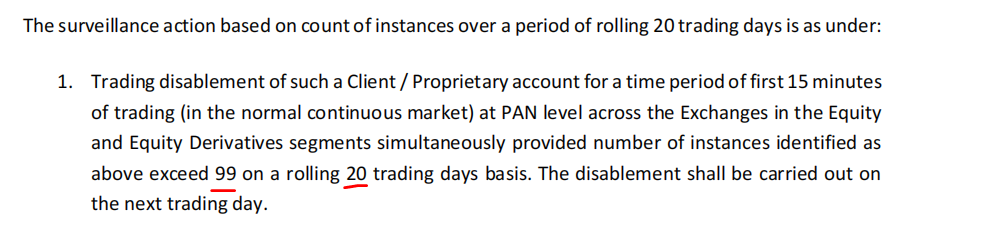

In continuation to the various surveillance measures in force, SEBI and Exchanges in a joint meeting have decided that, in order to further strengthen the order level surveillance mechanism, there shall be an additional order based surveillance measure to deter persistent noise creators i.e. excessive order modifications/ cancellations with an intent to avoid execution.

How will this impact the big guys? More importantly, will this cause widening of bid/ask spread in the index derivatives?

Any insights on how folks were gaming the system - which caused NSE to implement this?

Firstly, you need to understand couple of methods in which markets can be manipulated.

Spoofing & Layering

This is placing a large amount of buy or sell orders either at one price or at multiple prices (layering) to create an illusion of a sudden increase in demand (total bid volume) or supply (total ask volume). This sudden increase in bids/asks then gets other traders and the market to react preemptively which could get the scrip move in a particular direction. The only issue is that those orders that were placed were never meant to get executed. As soon as the market price gets close to the price at which these orders were placed, they will either be canceled or modified to a price further away. Hence spoofing the markets into believing that there is demand/supply and hence being able to maybe move the price of a security in a particular direction.

Quote stuffing

All exchanges have technical limitations in terms of how many orders the exchange matching engine can handle per second. When the number of orders are greater than this threshold, the exchange systems can slow down, not just for that one particular scrip but across the exchange. This slowing down could be for very small duration, just a few seconds to maybe even milliseconds. This slowing down will typically negatively affect high frequency traders doing arbitrage trades the most. Most of their strategies will lose money if they are slow.

Check this

Both these methods aren’t just manipulative in nature but can stress the exchange infrastructure. By the way some blame quote stuffing as the reason for the the 2010 flash crash on the Dow Jones.

In India we have had monetary penalty to ensure unnecessary orders aren’t placed on the exchanges. Last year there was a circular put out which penalized if the order to trade ratio was more than 50, ~Rs0.02 per order. This penalty has now been made a lot more - exchanges disabling the account from trading itself. The circular also says that even if the order to trade ratio is lesser than 50 and if found that orders are being deliberately placed without an intention to trade, the penalty can be applicable.

How does it impact?

This is positive for the markets and retail traders. Order to trade ratio of 50 is quite high and will cover for most of the genuine cases. It will mostly only affect those who deliberately were placing orders to manipulate the markets. At Zerodha we have never had a customer reach a 50 order to trade ratio.

Here is a nice idea - Maybe you can add a small feature on the executed orders page which displays this ratio(might be a good visual indication) so that the accounts don’t get disabled or maybe you can add this to your nudge feature which will give a pop up when you are nearing this limit . But anyways since nobody at zerodha has crossed that limit maybe this feature is not required.

Can you clarify this further please.

Is it 50 orders in the same script.

Say if someone enters 50 orders some buy, some sell in different stock symbols (say 25). and of these only one or none gets executed on the exchange. Would that still count as breaching the 50 to 1 ratio?

None of our customers over the last 1 year have violated this rule. I doubt any retail trader can, so don’t sweat about this. If you are placing orders that don’t get executed on a certain day, it won’t affect. This will most likely be an issue only if you are firing a lot of orders that don’t execute.

It seems you can only place SLMs that are 40%-50% away from the spot rate. I’ve seen this, so in order to stay very far OTM on the SLM, so my SLs don’t get hit - I could be placing 50% away, and then updating during the day as the market moves.

Just a scenario, not sure if this regulation will affect that, or will it affect algo traders, or those who are pinging the market to see where the roof / floors are on price.

Not sure. I’m referring to execution range, I’ve tried placing SLMs on my orders at 2x or 3x from my order. And it wouldn’t go through. I think this was execution range as per…

Spoofing the markets needs more explanation, let me explain with an example.

You may think what’s the benefit of the person spoofing the markets?

Ex 1: He has a lot of shares of a stock bought at 10, he wants to spoof the markets and when the price reaches 15 he will execute the order. Thus making an undeserved or unnatural profit of 50% in a short time. You can guess who loses here. RETAIL TRADERS.

Ex 2: He does not have any shares of a less traded stock still with good enough volume to make a profit intraday. He is spoofing the markets – shorting a huge quantity of stock then cancelling and bringing the price down further. When the price reaches a certain level he buys a lot of it. Then wait for RETAIL TRADERS to buy the stock. Price moves up. He exits and sells at a profit.

Ex 2 is exactly what happened in 2010 Flash Crash. Ex 2 is only possible intraday not positional. Ex 1 is done on a day the spoofer see good liquidity in the stock.

@nithin I think this rule should have come into effect a day after 2010 Flash Crash in all stock markets in the world. Thanks for the update. Is India first to do so?

What if someone places 50 orders on 50 different scrips and cancels them all? Or assume they were Mis orders and didn’t get executed any of them and broker cancelled them.

@nithin Every once when I come across these kind of news it just messes me up. Are there other circulars related to these order placement things from the exchanges and can you please share them, if there are any? It’s better to know things before venturing into unchartered territory.