There have indeed been instances when it has been considered that GOI breached the sovereign guarantee or was very close to breaching it.

-

The most famous example is the abolition of Privy purses. Even though the amount due was around 4 crores annually & it was guaranteed directly by the Constitution, the Govt of that time decided to do away with it. Nani Palkhivala summarizes that issue briefly (From 3:19 to 5:02)

-

SSNNL Bonds. This matter remains sub judice & doesn’t directly involve the central government (instead, a state government is involved). Here the interest liability is upwards of 12,000 crores (on the borrowing of 570 crores) as mentioned in an article. A separate article by Aarati Krishnan explains this issue well - Myth of sovereign guarantee.

-

The recent GST shortfall fiasco. Even though GOI shrugged off the responsibility of the shortfall on the GST Council and there was a political slugfest with accusations of a sovereign default, parallelly anticipating the shortfall will ultimately become GOI liability, well before GOI announced the extra borrowing of 1.1 lakh crore a week back, RBI had told banks that if they buy another 3 lakh crores of government bonds, those wouldn’t be needed to be marked to market (as mentioned in an article)

Most of them can be attributed to change in the policy outlook compared to when the sovereign guarantee was promised.

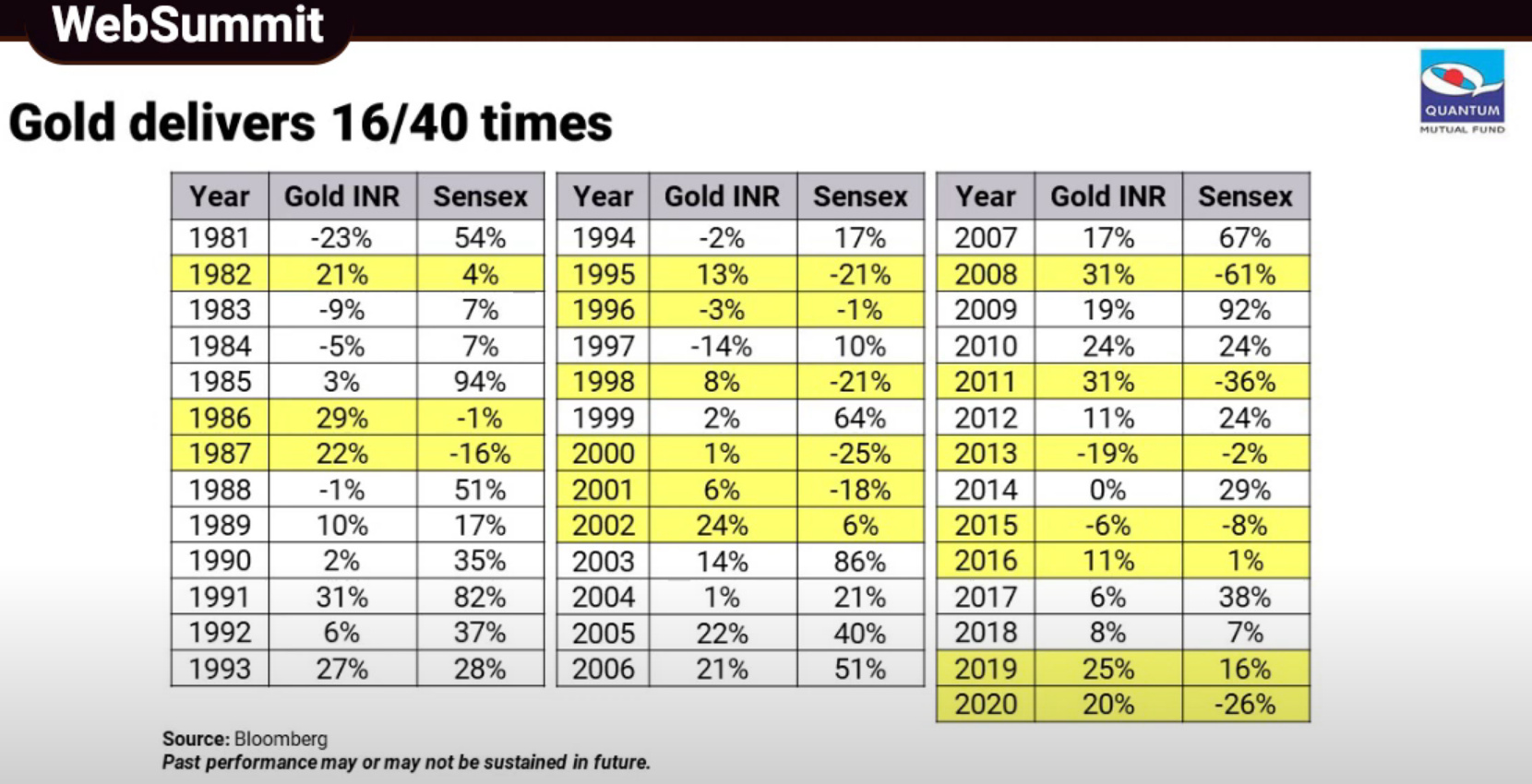

As per the 2019-20 RBI Annual report, a total of 9,652.78 crores (30.98 tonnes) has been raised through SGB (37 tranches) since its inception in November 2015 (Page 190). The gold price has appreciated around 80-90% since then (The price per gram was fixed at Rs 2684 in the first tranche whereas latest tranche had its price fixed at Rs 5051 per gram). Data about increase/decrease in gold prices in the recent past -

Hypothetical, even if all the money (9652.78 crores) was raised via the first tranche (which isn’t the case), even then the obligation on GOI would be approximately around 19,000 crores as per the current gold rate. Given that GOI raises over 40,000 crores on a weekly basis via auction of T-Bills (Issuance calendar for Treasury Bills) & Government securities (Issuance calendar for Government Bonds (G-Secs/GOI Dated Securities)), I don’t think GOI will have any issue in repaying back SGBs. Recently there have been auctions in which government securities have remained unsold but normally this doesn’t happen.

Also, if all else fails, RBI has gold reserves of over 650 tonnes, out of which around 100 tonnes have been added in the last 3 years (over 3 times more than total SGBs sold till last FY). Hence, even if gold prices go crazy, GOI does own the underlying asset and can just sell it directly to meet the obligations arising from SGB

But please keep in mind, these are all my speculations (more about this later)

GOI reserve isn’t only the taxpayer’s money. It has its own assets (around 17 lakh crores in form of land, equity, etc) and it is trying its best to raise money by selling them (Even though its disinvestment targets currently look unachievable).

But I agree that taxation is indeed a sweet spot for GOI, which it can tap into whenever it needs funds. The best example being the taxes on fuels (around 200% markup on the original price, with further hikes likely)

This website sheds some light on this -

The issuance of the Sovereign Gold Bonds will be within the government’s market borrowing programme for 2015-16 and onwards. The actual amount of issuance will be determined by RBI, in consultation with the Ministry of Finance. The risk of gold price changes will be borne by the Gold Reserve Fund that is being created. The benefit to the Government is in terms of reduction in the cost of borrowing, which will be transferred to the Gold Reserve Fund.

(ii). Bonds will be issued on behalf of the Government of India by the RBI. Thus, the Bonds will have a sovereign guarantee.

(xv). The amount received from the bonds will be used by Gol in lieu of government borrowing and the notional interest saved on this amount would be credited in an account “Gold Reserve Fund” which will be created. Savings in the costs of borrowing compared with the existing rate on government borrowings, will be deposited in the Gold Reserve Fund to take care of the risk of increase in gold price that will be borne by the government. Further, the Gold Reserve Fund will be continuously monitored for sustainability.

(xvii). The deposit will not be hedged and all risks associated with gold price and currency will be borne by Gol through the Gold Reserve Fund. The position may be reviewed in case ‘Gold Reserve Fund’ becomes unsustainable.

I am not aware if this original policy still remains in force or has been tweaked. But, if it remains the same, then it is indeed unlikely that the funds in the Gold Reserve Fund would be able to cover the price rise in gold since the first tranche of SGB. It is likely GOI will have to resort to some different method (like the speculations that I made above or something different) to meet the obligations from these bonds when they mature as GOI has explicitly assigned a sovereign guarantee to them.

I personally think, GOI meets its obligation towards investors by taking on more debt (I think this is how all governments in the world work). An example is NSSF (which manages PPF, NSC, SCSS, etc) which is around 17 lakh crores in size and is used for giving loans to FCI, NHAI, etc. In some cases, to service the first loan it has given, it gives another loan (Refer to the last paragraph of this article)

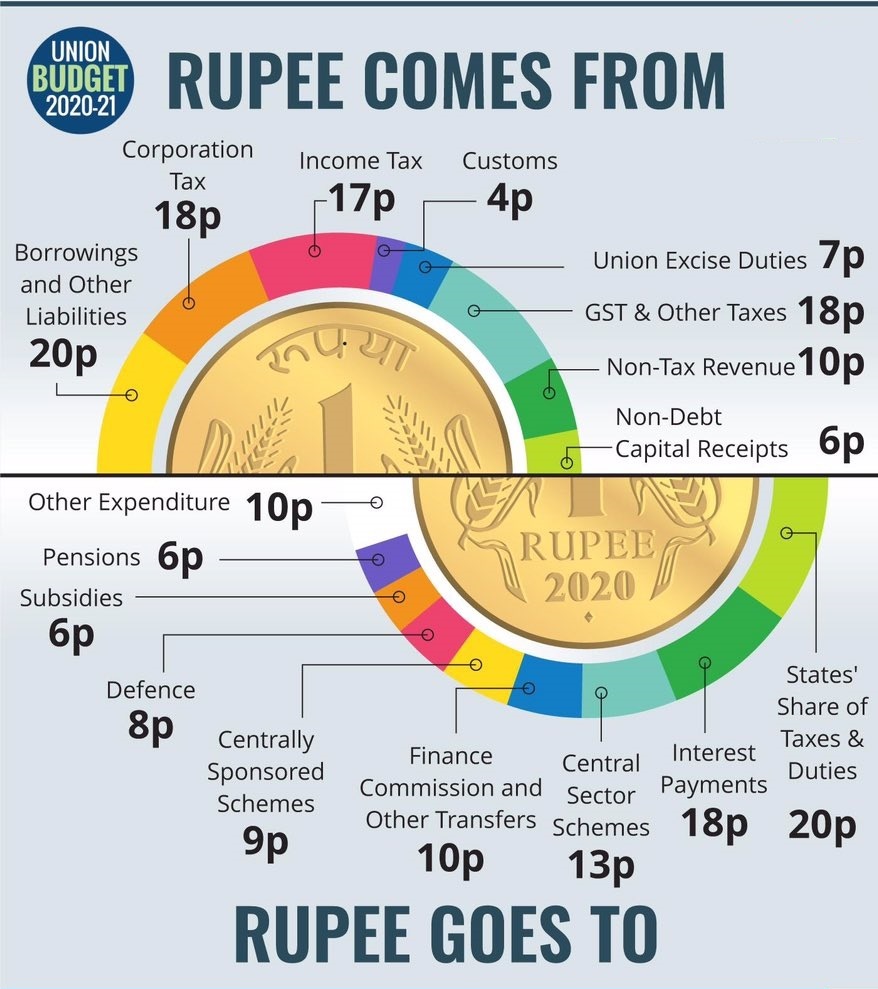

But if you are interested in a general breakdown of how GOI earns money, there is a graphic released with the Union budget which sheds light on that -

The amount of gold reserve of a country cannot directly strengthen the currency of a country because we don’t use Gold Standard monetary system nowadays. As we use a fiat money system, interest rate differential dictates depreciation/appreciation of the currency in the long term under normal circumstances (This concept is explained briefly by Abid Hassan in this video)