Recently I switched my shares/ bonds/ govt securities portfolio from HDFC Securities to Zerodha considering better UI of Kite, low expenses and features like Sentinel etc. Though, I have not yet shifted my mutual fund portfolio to Zerodha Coin.

I would want my entire portfolio, everything on a single platform but following are reasons stopping me to consider Zerodha Coin as Mutual Fund investment platform:-

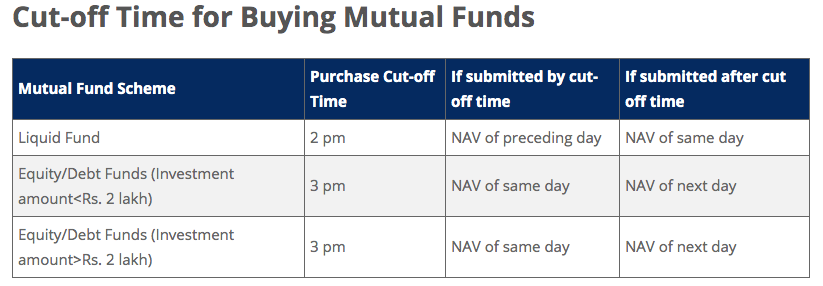

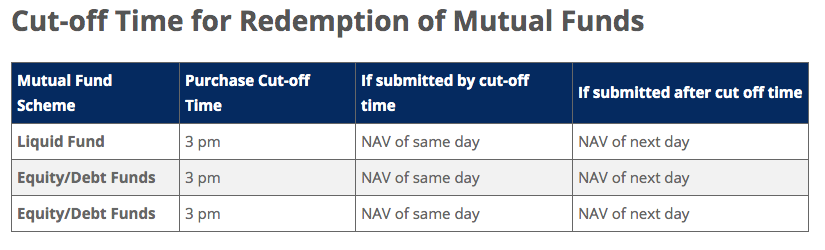

1. The cut-off time to buy/ redeem is strictly 1:30 pm on Zerodha Coin:

Whereas, Mutual Fund cut-off time is otherwise as mentioned below.

Zerodha Coin forces you to submit your order by 1:30 pm which may get you a different NAV than desired.

2. Unable to switch from one fund to another of the same AMC with same day NAV:

If you want to switch units from fund A to fund B within in the same AMC, you won’t be able to do it with same day NAV, because you have to first redeem the units from fund A which will take T+X days (depending upon the fund) and then you have to buy Fund B. So there would be difference in NAV in those T+X days. This is a demerit of having mutual funds in Demat format.

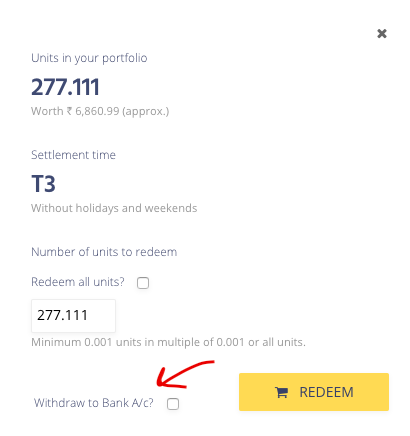

3. Credit of funds to bank a/c takes longer after redemption:

If order is placed before 1:30 pm, Coin would take T+X days (depending upon the fund) for the redemption amount to be credited to Zerodha trading account. Once the amount is credited to Zerodha trading account, you have to manually withdraw the amount so it is credited to your bank account. This takes upto 24 hours from the fund withdrawal request. So in total T+X days + upto 24 hours.

Tip for Coin product development team: Why not add a tick mark while redeeming so the user can select whether to withdraw the amount to bank a/c also so it saves them from manually doing it later.

4. No direct bank a/c to SIP. No STP:

SIPs on Coin are not usual SIP directly from bank a/c. You have to manually transfer funds to Zerodha trading a/c on or a day before of SIP or you can keep funds in the Zerodha trading a/c which means you lose on bank interest on the amount. Also, there is no STP option available on Coin.

5. Unable to avail benefits of Insta Redeem Liquid Funds:

Insta Redeem Liquid funds e.g. Reliance Liquid Growth, Axis Liquid Growth etc. funds allow you to redeem upto Rs 50,000 or 90% of your invested amount within as early as 30 minutes even at midnight or weekends. Though these funds are available on Coin, you won’t be able to redeem them instantly. It would take T+1 day for redemption (if order is placed before 1:30 pm).

6. Detailed Portfolio information not available:

On Zerodha Coin, it does not show detailed portfolio information and analysis e.g. percentage allocation amongst Large, Small, Mid etc, Percentage allocation between Debt and Equity, Total expense ratio and returns of the entire portfolio, sub-divided into debt portion and equity portion, Filter portfolio by fund type, AMC etc to analyse the performance on various parameters.

7. Doesn’t show units without any exit load, and LTCG tax-free units available for redemption/ switch:

Zerodha Coin does not show you the units available in a fund which won’t incur in any exit load upon redemption. Also, it does not tell you units available in a fund which have completed more than 1 year or more (along with their respective returns) which can be redeemed, switched, rebalanced without any LTCG and so the returns become tax-free. This information is quite handy while rebalancing your portfolio.

8. Can’t invest in NFO:

You can’t invest in New Fund Offering of a mutual fund scheme on Zerodha Coin.

9. Can’t pledge MF for margin or LAS (Loan Against Securities):

You can’t pledge mutual funds to create margin which can be used for equity delivery. Also you can’t avail loan against the mutual funds.

10. No information provided about the market or changes in the fund:

Coin does not provide you any information about the dynamics of the market. What are the indices changes weekly, resignation/ appointment of a fund manager, change in TER of a fund .etc. details.

Though Coin has recently waived off the DP charges for redemption, and earlier the Rs 50 monthly subscription charges were waived off for investments exceeding Rs 25,000, I believe the above mentioned pointers are important factors for an investor to consider and thus requires attention of @nithin, @faisr, and team Coin.