The yields on Govt bonds have risen substantially this year and there’s a lot of interest from investors. But we also get a lot of questions from investors about how Govt bonds work.

Let’s understand the basics in this topic.

The Govt needs money to finance various activities such as health, infrastructure, defence & other obligations.

So, the Reserve Bank of India (RBI) issues bonds on behalf of the central and state governments to raise money to fund these activities.

How are Govt securities sold?

The RBI conducts an auction where banks, primary dealers, mutual funds, and insurance companies bid on the bonds. A cut-off yield or price is then discovered at the auction based on which the bonds and T-bills are allotted.

-

Bonds with less than 1 year of maturity are called Treasury Bills (T-bills)

-

Bonds with more than 1 year of maturity are called G-Secs.

-

Bonds issued by state governments are called State Development Loans (SDLs).

How does a T-bill work?

T-bills are issued at discount and redeemed at par or face value. For example, a 91-day T-bill worth Rs 100 will be issued at Rs 98. After 91 days, the bill will mature, and you will get Rs 100.

Unlike bonds, T-bills don’t have any interest payments. The difference between the issue value and the maturity value is your return.

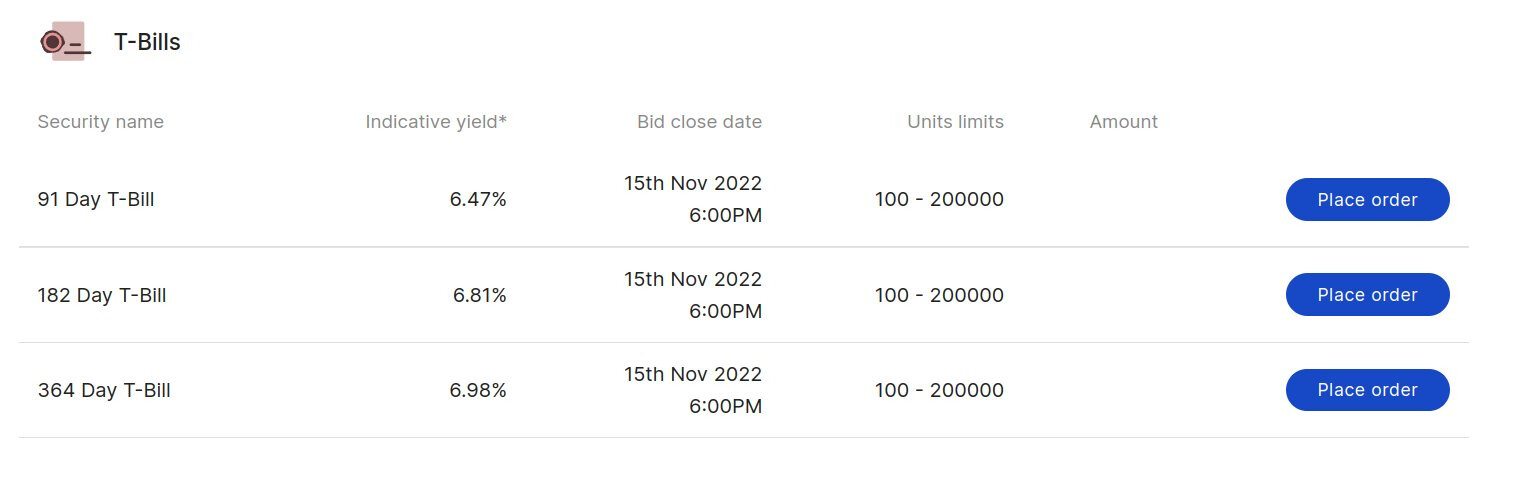

Here are the t-bills available for investing this week. One common question we get is, "will I get 6.5% for 91 days?

All returns are calculated on an annualized basis. As explained in this Varsity chapter.

Yield essentially measures the return on your investment on an annualized basis. After all, all investments should be measured by its returns on an annualized basis. So if you have made 3 bucks over 91 days on investment of Rs.97, then at this rate, how much would you have made every year?

The formula is –

Yield = [Discount Value]/[Bond Price] * [365/number of days to maturity]

= [3/97]*[365/91]

= 0.0309*4.010989

= 12.4052%

Once the T-bill matures, the money will be credited to your primary bank account.

How do G-secs and SDLs work?

Both G-Secs and SDLs are long-term bonds, and they are structured the same. Let’s first understand how to read a G-Sec/SDL symbol.

Let’s take the example of a G-Sec—7.10% GS 2029:

7.10% is the annual interest

GS is short for government security

2029 is the maturity year

It’s the same for SDLs:

8.64% MP 2033

8.64% is the annual interest

MP is short for Madhya Pradesh

2033 is the maturity year

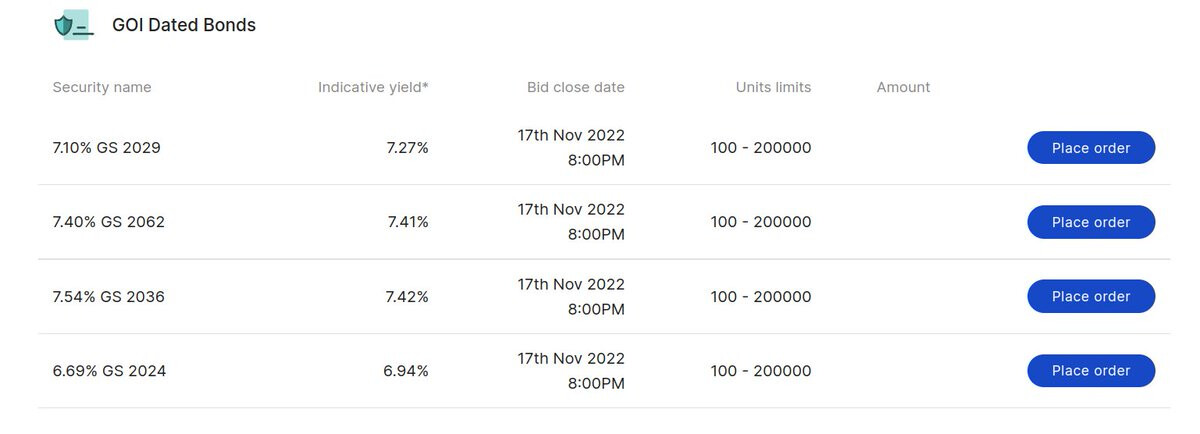

Here are the G-Secs available for investing this week.

If a bond doesn’t have an interest in the symbol, that means it’s a newly issued bond. The yield will be discovered in the auction and the interest will be the same as the yield for newly issued bonds.

How is the interest paid?

The interest is paid out semi-annually. It will be credited to your primary bank account.

At what price or yield will the bonds be allotted?

The yield or the price will be discovered through competitive bidding conducted by RBI where institutions participate. When you buy a G-Sec on Coin, you are buying it through the non-competitive bidding mechanism.

The bonds will be allotted based on the price/yield discovered in the RBI auction. Since the price is unknown, the exchanges block an amount in your trading account.

After the auction, the difference between the auction price and the amount blocked will be refunded.

How do I buy the bonds without knowing the price?

The prices discovered in the auction will broadly be around the current. On Coin, we show an indicative yield to give you an idea based on the current G-Sec, T-Bill, and SDL prices from RBI and CCIL.

https://ccilindia.com/OMHome.aspx

What’s the difference between yield and interest?

The interest of a bond is also called as “coupon”. When a bond is issued for the first time, the yield and the interest (coupon) will be the same.

Since all Govt bonds and SDLs are listed, their price changes. Yield or yield to maturity (YTM) is calculated to account for the price changes. You can use the “YIELD” formula in Excel or any other YTM calculator.

Here are the steps: Reserve Bank of India - Frequently Asked Questions

How do I invest in Govt bonds and SDLs?

You can invest on Coin here.

Can G-Secs, SDLs, and T-bills be pledged?

Only G-Secs can be pledged, and they are considered as cash component.

T-bills and SDLs cannot be pledged. See the list of G-Secs accepted for pledging here: What is pledging, and how does it work?

Is there anything I can read to understand more?

You can check out this Varsity chapter;

Taxation

T-bills

Since all T-bills mature within 1 year, STCG at your slab rate will apply.

Taxation on G-Secs and State Development Loans (SDLs)

-

Interest payments (coupons) from G-Secs and SDLs are taxed at your slab rate.

-

If the bond is sold within 12 months, Short Term Capital Gains (STCG) at your slab rate will be applicable.

-

If the bond is sold after 12 months, Long Term Capital Gains (LTCG) of 10% without indexation will apply. There’s no provision for indexation on Government Bonds.

Where do I check the upcoming issues?

You can check the upcoming issues below;

G-Secs: Issuance calendar for Government Bonds (G-Secs/GOI Dated Securities)

T-Bills: Issuance calendar for Treasury Bills