Earlier this year, i invested a small amount to purchase an NBFC bond at a discount to obtain 15% returns. I did this as a learning experiment to get a first-hand experience of purchasing a bond from the secondary-market (NSE exchange). As part of my due-diligence to review the company i was investing in, i read its prospectus and explored the products/services offered by the company on its website.

What started as simple curiosity about the company whose bond i was purchasing, soon developed into an obsession to understand the intricacies of the financial products they were offering.

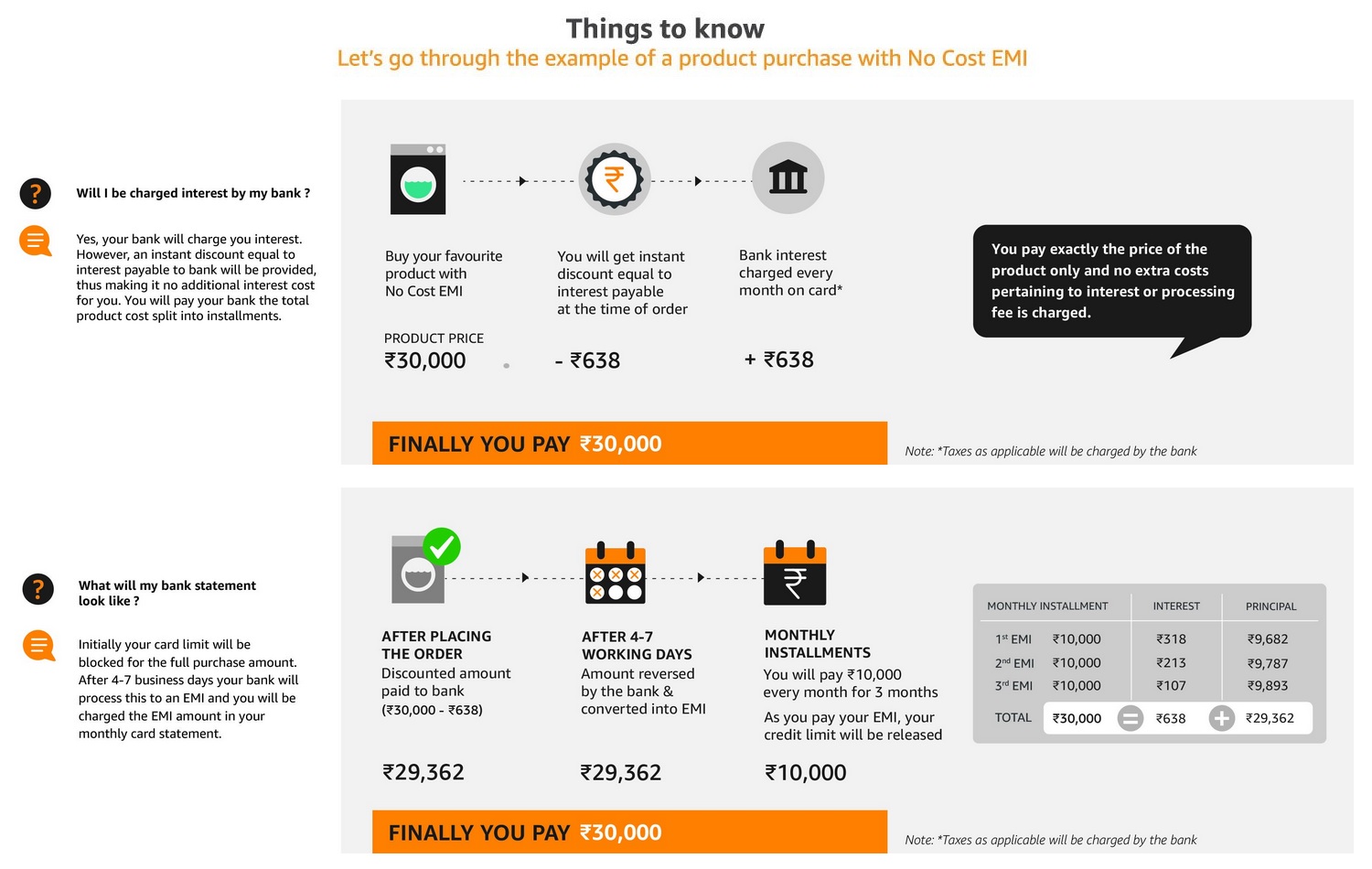

Here’s is a summary of what i learnt digging down the rabbit-hole that is zero-interest EMI loans.

Marketplace EMI Magic

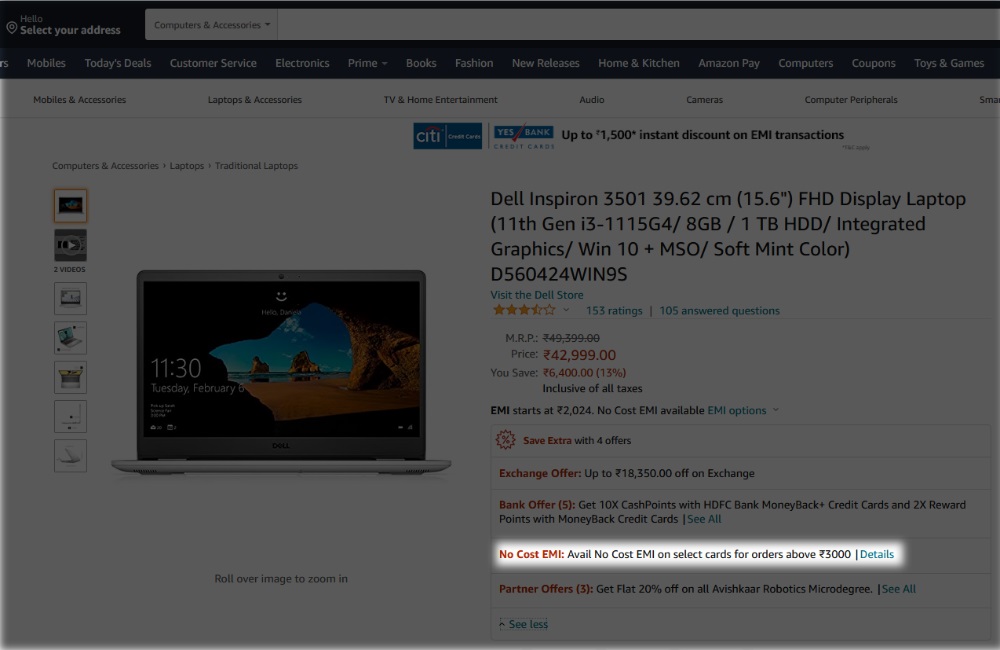

While browsing through online stores, you may have often come across typical zero-interest EMI offers.

Clicking on it to find out more details, you will be presented with an offer along the following lines.

[ Source: Amazon.in ]

In the above scenario, the seller of the product (to be accurate, the marketplace it is listed on) is bearing the cost of the loan which would otherwise have been paid by the buyer as interest on the loan. Also, behind the scenes, the bank might offer the seller/marketplace some kickback for promoting their loan offers for such transactions.

While this may seem like a good deal for the buyer, the seller/marketplace might be charging more (or offering a smaller discount) compared to the price offered if purchasing the same product with a full payment without any EMIs involved. Sellers/Marketplaces are smart enough to do this discretely by offering the identical product as a different SKU at a lesser price, but without the zero-interest EMI offer applicable on it.

Furthermore, as there’s a loan issued in the name of the buyer/individual which affects their credit-score, in case one claims a return/refund on the purchase, the seller/marketplace is now able to flag the loan as a default and ruin the individual’s credit-history/score. ![]()

Enter NBFC EMIs

Another common example of such zero-interest EMI offers are often offered by banks and NBFCs. Here’s an example of such a zero-interest EMI offer from Dhani Loans, the NBFC whose bond i had invested in, which got me interested to explore this domain in the first place.

[ Source: dhani.com ]

In this case, a marketplace/seller of a product is NOT involved. The user of the card can choose to purchase anything online/offline and avail an effective loan repayable in 3 EMIs. So, how can the NBFC afford to provide such loans at zero-interest and still make a profit?

The simple answer is usually processing fees. NBFCs charge a fixed amount (or sometimes even a percentage) of the loan/credit amount as processing fees. A processing fee between 1-2% does not seem like much. However, remember that these loans are for extremely short periods mostly between 6 weeks to 6 months. Thus, the effective annualized rate of returns from the processing fees alone can be effectively between 4-8%.

But, Dhani proudly claims “No processing fees” on their OneFreedom card. Also Dhani’s cost of capital is 10-11% - i.e. the dividends they pay on the corporate NBFC bonds they used to raise the capital they lend. How can they afford to raise money at a higher-rate and lend it forward at a lower rate?

Well the Dhani Freedom card we saw above is NOT their only product.

They also offer the typical personal and business loans at 12-17% (or even higher).

[ Source: Dhani Loans ]

During the pandemic, Dhani has also diversified by launching its own online pharmacy and daily-goods marketplace. Overall, Dhani looks like an opportunistic player trying to make a buck wherever it can.

So what’s the catch?

Coming back to Dhani’s OneFreedom card that offers 0% interest EMIs as no processing fee. Does it mean that the OneFreedom card is a loss-leader venture Dhani is using to gain market-share and the goodwill of its customers? No, NOT AT ALL. In fact, the reality is quite the opposite. Dhani’s OneFreedom card offering 0% interest EMIs might possibly be its most profitable venture. Let us explore how Dhani does it…

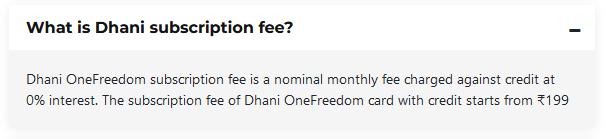

Though there is no interest levied on the EMIs, nor are there any processing fees, there is another aspect to the Dhani OneFreedom card using which Dhani is minting money - The monthly subscription fee.

[ Source: Dhani OneFreedom FAQs ]

While Dhani downplays the significance of the subscription fee on its website,

the math behind it clearly paints a different picture. Here’s an example…

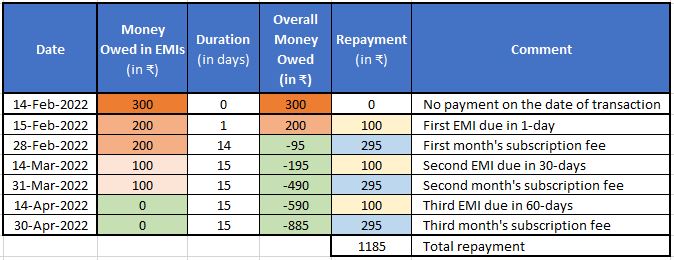

Every spend you make using Dhani OneFreedom is automatically converted

into 3 interest-free installments spread over 60 days.For example,

You make a transaction of ₹300 using a Dhani OneFreedom card on 14 February 2022.₹300 gets automatically converted

into 3 interest-free installments which you have to pay on

Day-2, Day-30, and Day-60 from the date of your transaction.i.e. you need to pay 3 installments of ₹100 each on

- 15 February 2022

- 16 March 2022

- 15 April 2022

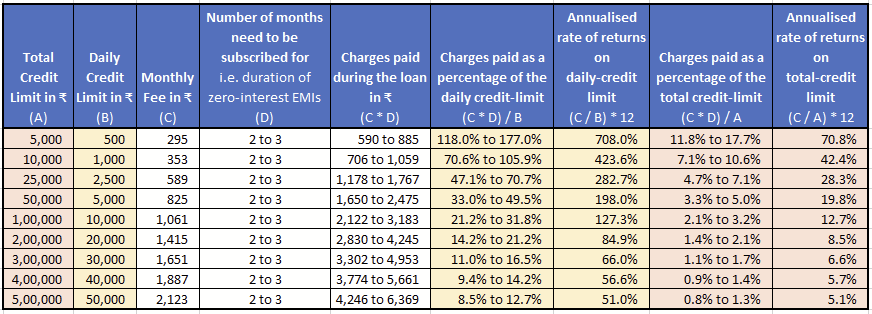

In addition to the above EMI payments, to be eligible for this credit-line/loan, one needs to pay the monthly subscription fee for the months of February, March, and April 2022. The monthly subscription fee depends on the credit-limit that one qualifies for. To qualify for the above transaction of ₹300 to be paid in zero-interest EMIs, one needs an overall credit-limit of atleast ₹3,000. This is because Dhani enforces a daily credit-limit of 10% of the overall credit-limit of an user of the OneFreedom card. To have an overall credit-limit of ₹3000, one needs to qualify for the ₹5,000 credit-limit “bucket”, that has a monthly subscription fee of ₹295 (₹249 + 18%GST).

[Sources: 1 | 2 | 3 ]

Thus, in addition to the 3 EMIs paid over 60 days,

an additional ₹885 is also paid as the monthly subscription fees (₹295 x 3-months).

A total repayment of ₹1,185 in ~2.5months for an initial credit/loan of ₹300!

i.e. an effective APR (annual percentage rate) of ~1435% !

Note1: APR = (₹885 / ₹300) * (365days / 75days).

Note2: Notice how despite using a daily-credit of only ₹300, one is expected to pay for a daily-credit-limit of ₹500. This is the main reason why the APR for the above scenario is even higher than the APR shown in the above table.

The above calculated APR, extremely high as it already is.

it still does NOT emphasize how truly bad it is for the borrower.

To get a better picture,

let us look at the repayment schedule of the above scenario…

Even though Dhani claimed to provide a daily-credit-limit of ₹300,

the way the EMIs are structured,

one ends-up repaying 1/3 of the credit/loan within a single day!

Also, even though the amount of loan/credit actually availed is lesser than the credit-limit,

the monthly subscription fee is paid as per the “bucket” of credit-limit one belongs to.

There is no relief in the monthly subscription fee for NOT utilizing the total credit limit one was eligible for.

Thus in the above scenario,

one has to effectively repay the entire loan amount within 15 days of obtaining the loan.

…and continue to repay ~3x more over the next 2-months!

If this isn’t a predatory loan, what is!

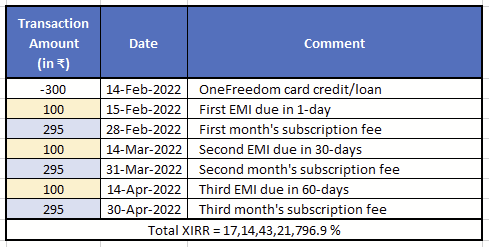

An excellent way to demonstrate using numbers, the craziness of this scheme,

is to calculate the XIRR of the above repayment schedule

using MS-Excel which is as follows…

Is that 1,714 Crore percent?? ![]()

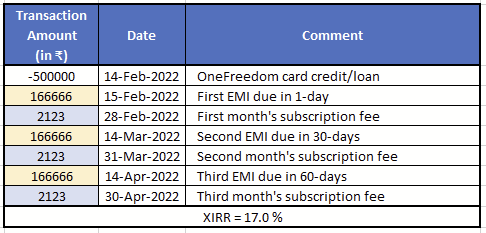

The situation is better in the higher “buckets” of credit-limits.

The absolute best rate one could theoretically get from the Dhani OneFreedom card is a 17% XIRR.

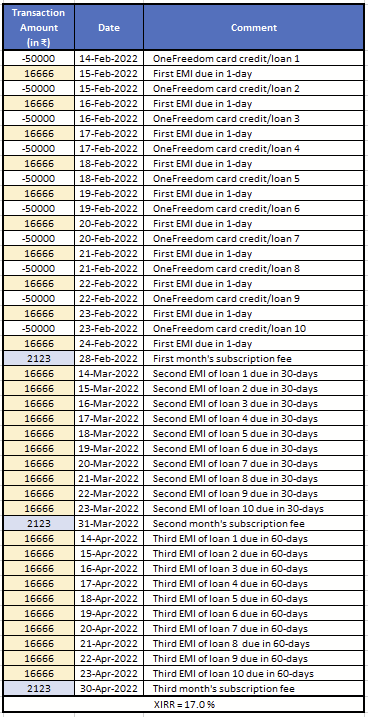

NOTE: Technically the entire amount of ₹5,00,000 cannot be availed as credit on a single day. Due to the daily limit, it has to be spread out over 10 or more days in the month. However, the effective XIRR in both the cases is the same 17% XIRR. Hence, for the sake of simplicity, the simpler schedule/table is shown above. For reference, here’s the actual detailed schedule/table.

{kind=link}

However to achieve this “best-case” 17% XIRR,

- One must first qualify for the highest credit-limit bucket (not clear what Dhani’s criteria are).

- One is still limited to ₹50,000 worth of transactions per day.

- One must make 10 (or more) transactions to utilize the credit-limit of ₹5,00,000.

- One must already have 33% (₹1,66,000) in-hand for down-payments.

- Technically not down-payments, rather the 1st-EMIs due on T+1 day of each transaction.

- One needs to have ₹2,123 in the account each month when the monthly subscription fee is due.

- One must NOT miss any of the above manual repayments (that’s right, no auto-pay/auto-deduct!).

- Otherwise, one is locked-out from any further credit and faces compounding penalties.

(until all the dues are repaid) .

- Otherwise, one is locked-out from any further credit and faces compounding penalties.

And by doing all this without fail, month after month,

one gets the “privilege” of paying back Dhani an effective 17% XIRR.

Quite a tall-order,

- one that most people are unlikely to qualify for,

- and even if they do, they’re likely to miss once in a while.

…and that my friends,

is how a zero-interest EMI loan

can earn returns of upto 1400% APR! ![]()

Author’s Note - Though i have checked all the various calculations above thrice for any mistakes/typos, there is a possibility i may have misunderstood/overlooked something. In case you notice a discrepancy, please share them in a comment below and i will be happy to fix it.

References / Recommended Reading