The penalty for intraday peak margin violations is going live from Dec 1, 2020. This regulation is going to affect intraday traders. Since intraday traders generate the maximum volumes and revenues, this will affect the entire brokerage industry significantly as well.

Firstly, what is the regulation?

I had explained this earlier, do check this post for details.

Here’s the gist: Until now, brokerage firms could offer any amount of intraday leverage, and now we cannot. Starting Dec 1, there is a maximum intraday leverage that can be offered. Also, this maximum intraday leverage will keep going down from Dec 1, 2020, to Aug 31, 2021. And from Sep 1, 2021, the maximum intraday leverage will be equal to the SPAN+Exposure margin for F&O (Equity, commodity, currency) and VAR+ELM(with a maximum 20%) for stocks.

What is SPAN+Exposure & VAR+ELM?

This is the minimum margin that exchanges ask brokers to collect from the clients on an end of the day basis for any open position today. If this margin is not collected, there is a penalty on whatever margin was collected short also called the short margin penalty. This penalty can be in the range of 0.5% to 5% of the shortfall per day.

- Here is the VAR+ELM margin for stocks.

- Here is the SPAN+Exposure margin for futures.

- Here is the link to our margin calculator where you can check the SPAN+Exposure for all F&O contracts (Equity, Commodity, Currency)

What changes post peak margin penalty?

Since margin reporting was happening only on an end of the day basis until now, brokerage firms were allowing customers to take intraday positions with margins far lesser than VAR+ELM or SPAN+Exposure. But these additional intraday leverages offered through products like MIS, BO, CO, etc. would forcibly be squared off before the close of trading hours, ensuring there is no margin penalty on the end of the day open positions.

For example,

- If Reliance VAR+ELM is 20%. Instead of asking Rs 20,000 for a Rs 1L Reliance intraday trade (MIS, CO, BO), some brokers would ask for only 5% or Rs 5,000.

- If Nifty futures require SPAN+Exposure of Rs 1.5L, brokers would allow customers to trade intraday with say just 30% of this amount or Rs 50,000.

The issue here is that when a broker collects a lesser margin than the minimum, the broker is taking additional risk. These margins are collected to protect the broker from client defaults. For example, if a broker allows a customer to trade for Rs 1L with only Rs 1000 or 1%, if the stock moves say 10% instantly, the customer loses Rs 1000, but the broker loses Rs 9000 (until the broker is able to recover the money from the customer). Competition forced some brokers to attract clients by offering excessive intraday leverages (50 to 100 times). This caught the attention of the regulator, especially after the issues at Karvy, BMA, etc.

So, to fix this for good, SEBI has introduced the concept of peak margin penalty. Similar to how a margin penalty is calculated if the margin collection is lesser than the minimum for the end of the day position, the same logic will now be used to calculate margin penalty if the available margin is lesser than the minimum SPAN+Exposure (Equity, Commodity, Currency) or VAR+ELM margin at any point during the trading day (intraday).

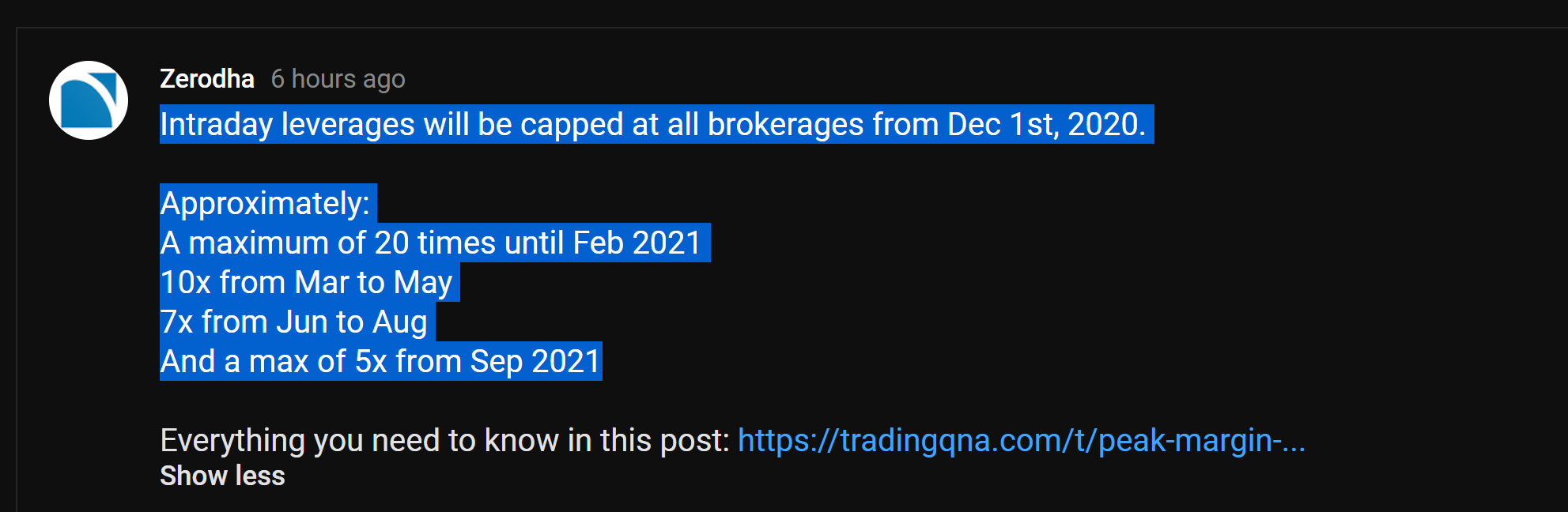

But since this practice of additional intraday leverages has been there for many decades, SEBI has given enough time for the industry to adjust. The circular was put out in Aug 2020 and from Dec 2020 to Sep 2021 the restriction will be slowly increased.

- Dec 2020 to Feb 2021 — penalty if margin blocked is less than 25% of the minimum 20% of trade value (VAR+ELM) for stocks or SPAN+Exposure for F&O.

- March 2021 to May 2021 — penalty if margin blocked less than 50% of the minimum margin required.

- June 2021 to Aug 2021 — penalty if margin blocked less than 75% of the minimum margin required.

- From Sept 2021 — penalty if margin blocked less than 100% of the minimum margin required.

The minimum margin as I said earlier is VAR+ELM for stocks and SPAN +Exposure for F&O. This minimum margin inherently has leverage, but there can’t be any additional leverage over and above this.

How does it affect us & the Broking industry?

At Zerodha

Equity

- In terms of number of trades: Intraday products contribute 55%

- In terms of traded volume: Intraday contributes 70%

F&O

- In terms of number of trades: Intraday products contribute: 40%

- In terms of traded volume: Intraday contributes 40%

Until Feb 2021, we will not be affected directly as the leverages we offer won’t change. But post that and especially after intraday leverages are completely removed by Sep 2021, our intraday business (above) I think will be negatively affected by at least 30 to 40% which can potentially mean around 20 to 30% hit in terms of overall revenue.

Rest of the broking industry

There are brokerage firms who have used additional intraday leverage to attract customers. So higher the intraday leverage offered by a broker today, the more that business will be affected. The lesser the leverage, lesser the effect.

How will it affect trading?

Intraday trading contributes significant liquidity to the markets. With restrictions on intraday leverage, the liquidity is bound to reduce and hence the potential impact costs for everyone might go up. But, high leverage is what usually destroys traders, and without such high leverages, the chances of a trader surviving markets will go up significantly. So hopefully the higher number of traders participating at any time will make up for the drop in liquidity.

My take on if intraday leverage should be allowed or not?

VAR+ELM or SPAN+Exposure margin computation doesn’t consider the difference in terms of risk based on if the market is open or closed. The highest risk is usually for an overnight position when the market can move significantly to factor in all the news from around the world at the market opening the next day. Hence VAR+ELM and SPAN+Exposure is justified.

But this risk reduces when the market is open as risk management engines of brokers can exit positions based on margin available and marked-to-market (MTM) losses. So maybe brokers should be allowed to offer some additional intraday leverage (some cap so it isn’t misused) over and above SPAN+Exposure or VAR+ELM as long as it is funded by the broker’s own capital.

But yeah, lower leverages while it might be negative in the short term for brokers & intraday traders, it is positive for the long term as the probability of intraday traders winning will improve with lower leverages.