@nithin what’s the reason behind the exchanges putting out this clarification now? Why not before? Also, wouldn’t Zerodha lose a lot of revenue, why aren’t you opposing this? When will other brokers adjust to this?

5 Likes

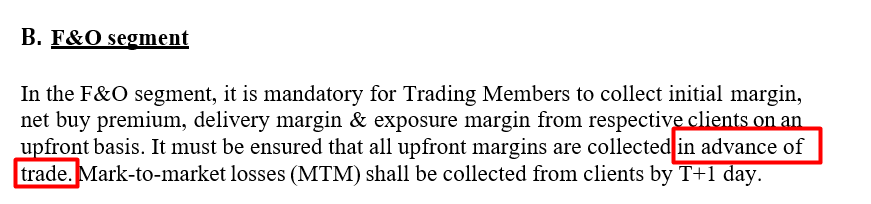

Firstly, the upfront VAR+ELM margin requirement for trading stocks that was introduced is new, but the upfront margin for F&O had always existed. Just that brokerage businesses including us had taken a view which was business-friendly. Let me explain -

For those who didn’t know - when a client buys 1lot of Nifty with only Rs 25k using an intraday order type (BO/MIS/CO) when the NRML (SPAN+exposure) margin is Rs 1lk, the exchanges block Rs 1lk from the broker. What this means is that the broker ends up funding the customer for the remaining 75k. If you are wondering why the broker allows the client to leverage, it is obvious - higher brokerage. Most traditional brokers charge a % fee, so the higher the value of trade, the more the fees. Even the flat fees broker (like us) will see a higher number of trades and hence revenue if the client has this additional funding/leverage. There is also the pressure to offer additional leverage fearing customers would move to the competition.

There are two issues with this -

- What if the 75k didn’t belong to the broker, but was of another customer? We as Zerodha have always put our own capital whenever a customer had traded without sufficient margin. But the recent issue with BMA and Karvy revealed to SEBI that they were blatantly using one client funds to fund another.

As you would imagine, if one client’s fund is used for another to trade F&O with high leverage, money can be lost really fast. If the broker isn’t sufficiently capitalized, this brings a big risk to all the customers with the broker.

For example, assume a client is long 10lots of stock future of contract size 10lks (lot size 10000, price 100), whose SPAN+Exposure is 20% or Rs 2lks. Assume this broker is allowing intraday trade with 5 times leverage or asks for only 4% or Rs 40k per lot or Rs 4lk to take a position worth 1 crore. Assume there was bad news on this stock and it fell 20% or Rs 20. Stop losses didn’t trigger as the fall was instant. This client would have lost Rs 20lks with only Rs 4lks present in the account, a debit balance of Rs 16lks. What if the client didn’t make good of the loss? What if it was not one client, but many clients? What if the broker didn’t have his own capital but was using another client’s idle funds to fund this client position? As you’d imagine, it creates a systemic risk. Even with 20%, there is no guarantee that it is enough when shit hits the fan (like in 2008), that is a risk every brokerage firm runs at all times, but SPAN+Exposure margin covers for majority of the risk and it also helps that it is updated 5 times a day to cover for even the intraday volatility of the stock.

- Regulations don’t allow brokers to fund clients for F&O. So you might have a question, how was it offered until now then?

All brokers are required to report client margin at the end of the day to the exchange. This reporting also ensures that one client funds can’t be used by another client, at the end of the day. If clients margin is lesser than the margin required to hold the position, there is a short margin penalty levied. So if a client held one lot of Nifty with just 25k while the required margin is 1lk at end of the day, there would be a short margin penalty on 75k which is quite a bit. This is where the brokerage industry took a view which favoured the business. Since the reporting is at the end of the day, there is no issue if there wasn’t sufficient margin intraday, as long as by the end of the day the position was squared off. Since no regulation specifically blocked this, everyone offered intraday products like MIS, BO, CO, etc with higher leverage or lesser mandated minimum margin requirement. This got fixed when exchanges put out the clarification maybe on behest of SEBI after the Karvy, BMA incident -

They now say margin has to be collected before the trade along with saying upfront margins leaving no more ambiguity. Hence the entire margin (SPAN+Exposure) for any type of derivative trade has to be present in the trading account before a trade. I am guessing there will be a penalty structure on this very similar to how it is for the end of the day basis in the future.

Going forward, the margin and reporting system for equity will be exactly like F&O explained above. So while trading stocks instead of SPAN+Exposure, the client will need to have the VAR+ELM margins.

I guess over the next few days. The exchange guideline is already out and on their website.

We have the largest community of retail traders, we will probably be the most affected brokerage in terms of revenue. But if you go through the explanation above, there is no real way to oppose it, is it? Also once it is put out as a rule, the penalty for breaking rules for brokerage firms is quite high. Us discussing it openly is atleast getting all brokers to put an effort to see if the rule can be changed. Keeping quiet isn’t a solution, it would eventually end up being stopped without anyone getting a chance to protest.

One of the things that SEBI has done with the recent circular on margin collection and through this clarification from the exchanges is to ensure that a client can only trade with his/her own funds only to the extent allowed. Forget other client funds, but the broker can’t put his own funds to fund the client as well. Maybe the broker should be allowed to intraday fund using their own capital if they are ready to take the risk and that is something we have been asking for. But this requires changes in derivative product design at SEBI, which is extremely tough, especially in an environment where the industry is hurting due to regulatory pressure after the incidents at Karvy and BMA. Hopefully we will soon have the good news of margin requirement dropping drastically for F&O positions that hedge each other.

Hopefully, this helps.

Cheers,

12 Likes

Nithin, just wondering how leverages work in US markets, I came across FINRA rules on intraday trading leverages and minimum capital required to be a intraday trader, the rules are brutal compared to India, it says minimum 25k USD is required to be a intraday trader and max 4 times leverage is allowed. So, how volumes are driven in those markets in spite of such low leverages? do you think with reduction of leverages in India liquidity will dry up and slippage will increase? This is a common query of many, hence asking here.

5 Likes

Yeah, thanks for sharing the FINRA link. I keep hearing about how US markets allow much higher leverage, it isn’t true. You can check this post which explains about buying power in the US

Like you said, for day trading, it is maximum 4x with minimum $25k account size. For futures it is 10% or 10 times for S&P E-mini, which is very similar to Nifty here.

US is a much more mature market than India with a lot more different type of participants, don’t really know if we can compare US to India. Not really apples to apples.

Will liquidity dry up and slippages increase?

Almost 85% of all trades are on options. Buying options won’t get affected, people who typically short options are people with access to more capital or stocks to provide for margin, don’t see that getting affected that much as well. With the new margining system planned, I think a new breed of people who trade option strategies vs trading naked will come to the scene. Stock futures might get affected, but in an algo world, programs will ensure that prices of underlying and future are in sync especially with physical delivery on stock future contracts.

Also

38% of turnover comes from Retail and HNI. Assuming 1/3rd or even 1/2 of them are retail who take additional leverage intraday and this reduces, this isn’t going to make too big a difference for liquidity or increase slippage.

While yes, I fight with regulators to allow us to provide leverage due to client demand, my general sense after being in the markets for over 2 decades is lower leverage is generally good for everyone in the long run while it is going to be extremely painful for the brokerage businesses like us in the short term.

9 Likes

@nithin when the hedged option strategy margin requirment will implemented , if thats will be here means every one will be happy ,not bothered about other things , SEBI is shutting all the doors is not good for any body

1 Like

After Sebi and BJP goverment, everybody lost peacefull sleeping nights in india , retail investor are fighting with

Trading QNA

3 Likes

Atleast they should not implement the VAR+ELM margins in Equity (cash) for (BO/CO) product types as the orders are safe with stoploss…

3 Likes

I am hoping in the next 3 to 4 weeks there should be some news.

4 Likes

The issue with stoploss is that it doesn’t guarantee execution and margin requirements are usually calculated based on the worst case scenario. Check this link to see the logic behind VAR and ELM.

Let me give an example.

Say stock A is trading at Rs 100, you buy at 100 and stoploss at 95. Assume there was some bad news and stock fell to 90. Assume this stock has a circuit limit of 10%, which now means that at 90 there are only offers to sell and no one bidding to buy. Yes, your stoploss would have gotten triggered at 95, but the time the sell order was placed, the market is already at 90 where it can’t be sold as there are no buyers.

This will lead to short delivery and an open risk for the broker until the shorts can be covered in auction on T+3 day. If you had say only 4% margin, any price below 96, the broker is losing his own money.

Now, you might think that you are a small retail trader who is doing for a few thousand or lakh rupees, so what big risk. But imagine there was this trader who did this for say stocks worth tens of crores. Potentially the broker can go bankrupt, risking all his other clients as well.

9 Likes

I have not seen any default of big broker in past ten years because of the above reason if things are working fine in the past even with high leverage then why to change it at all?

4 Likes

There have been a bunch of defaults in the recent past which has triggered all of this - BMA, Allied, etc. Check this list. But after the Karvy episode, things are really changing fast.

Rules are made for bad actors and it ends up affecting everyone.

5 Likes

worst move ever.

we had to stop trading in commodities because they removed all mini contracts, now this move.

RMS of zerodha closes the position automatically if there is shortage of funds.

the worst case scenario is kind of w black swan event and for that killing so many retail traders is not justified.

zerodha has the maximum no of retail traders, they should do something.

3 Likes

Should a regulator form rules based on outlier / extreme events ?

There will be bankruptcies of companies and individuals when doing business. Why create hurdles for human endeavour ? Instead regulators should focus on making rules for cleanup after a mess happens. Risk is inherent to business !

8 Likes

Hi Nithin,

So there will be no difference between mis order and normal order other than mis order gonna exit the position same day.

Very clear explanation…

I don’t know why all oppose for VAR+ELM margins in Equity.

It’s good to curb SPECULATION which are done by over leverage on Equity.

And for F&O SEBI already working definitely good news will come.

NOTHING to worry about if all think properly about this, It is very good step.

Am sure @nithin thinking how to Explain fellow traders.

you should proud about ZERODHA for providing clean ,peaceful & secure ENVIRONMENT.

2 Likes

@nithin

On a personal note should I be as a professional investor be benefited with it in long term because all my trades are NRML type but in expiry day I did write options by converting my NRML to MIS and reverting it after 3:00 pm. which provided me with extra float , is there turnaround to it.

1 Like

Yes, in case of fno, but in equity still intraday leverage up to 8 times can be available.

1 Like

Hopefully, but once sebi comes out with new margins for hedged positions required margins will go down drastically for those positions. On day of expiry also full margin is required, no turnaround on this for now as I know.

I am grouping bunch of your questions and answering same time.

Like I explained in my original post, no margin amount guarantees that the risk is covered. But more the margin lesser the risk for the industry. Regulators would generally want lower risk in the ecosystem.

There is no conspiracy theory to stop anyone from shorting options.

About lower margin for hedged positions, it is not more than a few weeks away.

4 Likes