If a member of the huf give interest free loan to his huf , does plain paper or the stamp paper agreement is needed ? Also , it needs to be notarized or not ?

If the loan is taken from an outsider/ friend to the huf , in that case notary is needed or not ?

If an MTF (Margin Trading Facility) buy order is short-delivered, the pledging confirmation will fail on T+1 due to the absence of holdings. The position will then be converted to CNC (Cash and Carry) holdings and settled either through cash or available holdings after the auction.

Zerodha Options Buy - first cash will be used for option buys and once there is no free cash then only collateral is used for option buying.

When We use collateral margin for option buying, Delayed Payment Charges (DPC) of 0.05% per day (₹50 per lakh) or 18% per annum apply only to overnight positions. DPC is charged only on the collateral amount utilised for option buying, not the entire option purchase amount.

refer article : Can I buy options using collateral margin?

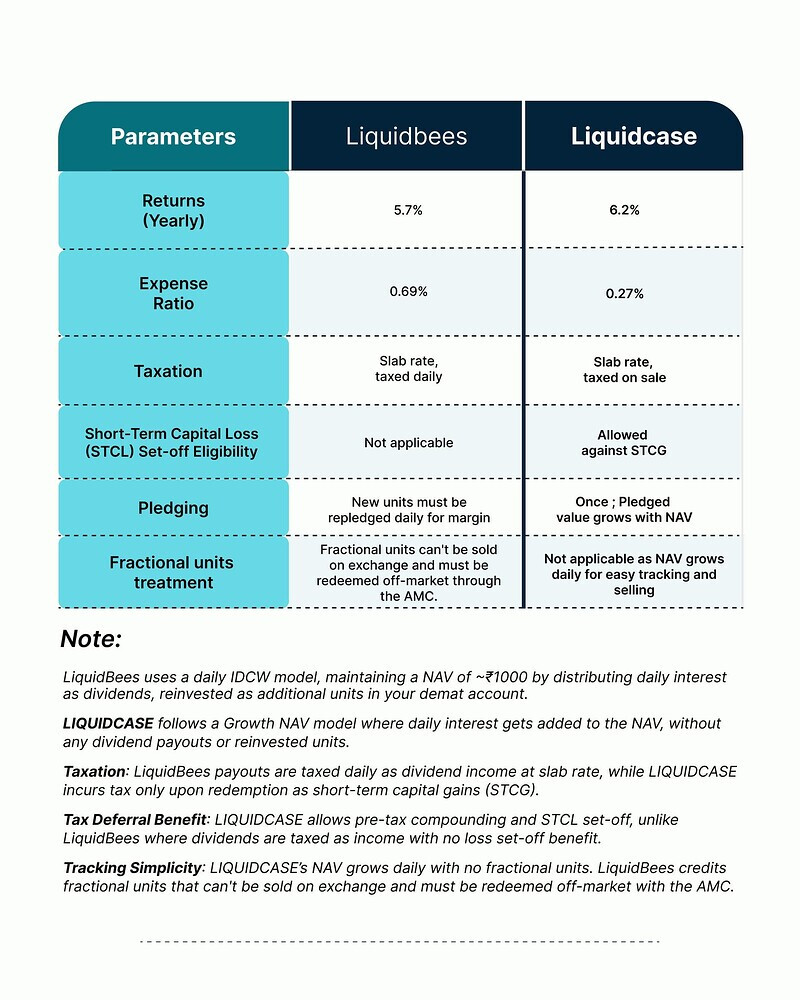

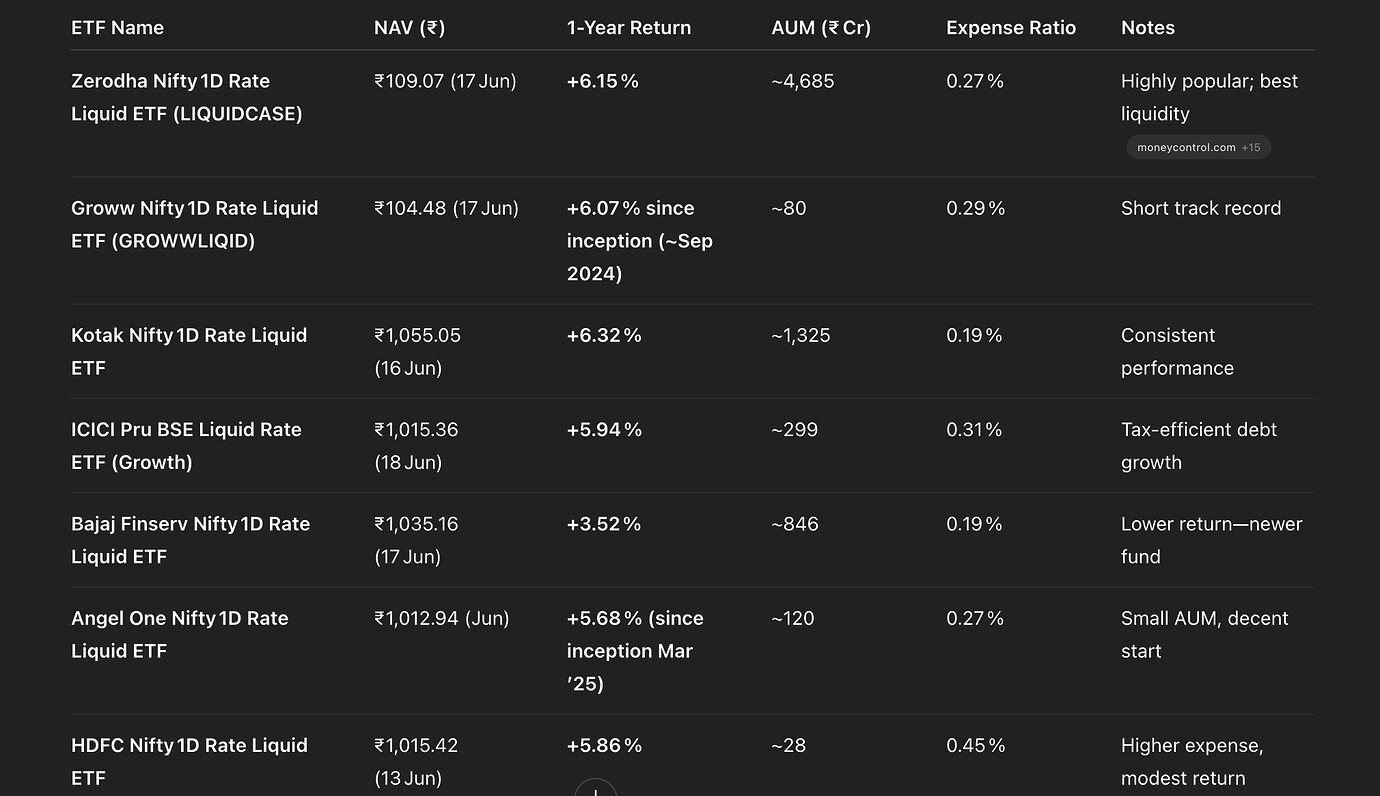

Zerodha took a commendable step by launching LiquidCASE , a Nifty 1D Rate Liquid ETF - Growth option , offering investors an ultra-short-term parking vehicle with daily compounding benefits and no daily dividend hassles.

Traditional options like LiquidBees pay out daily dividends and adjust units, which may:

Increase backend complexity for AMCs (unit adjustments, reinvestment logistics)

Cause tax inefficiencie for investors due to regular dividend income

Result in fractional units that are difficult to sell in the secondary market

Growth structure simplify tax and accounting for both the fund house and investors.

Since there’s no daily dividend, it defers tax until sale, avoids fractional issues, and may be more cost-efficient for retail investors.

Zerodha’s LiquidCASE growth format gaining high traction suggests strong user demand.

For traders, the growth mode enables smoother automation, SIP/STP, and system-based strategies without worrying about dividend reinvestment.

For tax-conscious investors, capital gains on exit (rather than regular dividend taxation) is often preferred.

India’s Reserve Bank (RBI) has shifted its strategy by draining excess cash from the banking system. On June 27, it’s set to conduct a ₹1 trillion (VNVRR) seven-day variable-rate reverse repo auction—the first time this has been used since November—to absorb surplus liquidity and realign short-term rates. This signals a move away from its prior stance of frequent liquidity infusions.

Key Points

Liquidity Drain via VNVRR

RBI to auction ₹1 trillion through a 7-day variable-rate reverse repo on June 27, withdrawing surplus cash from banks (moneycontrol.com).

Policy Tool Resurgence

It’s the first use of this tool since November, indicating a marked shift from liquidity addition to absorption (moneycontrol.com).

Record Liquidity Surplus

The banking system holds an excess of around ₹2.3–2.4 trillion as of June 23 (reuters.com).

Impact on Short-Term Rates

Reverse repo withdrawals aim to push overnight call rates closer to the repo rate, countering them staying near the lower Standing Deposit Facility (SDF) rate (reuters.com).

Temporary Halt to Fortnightly Operation

RBI will skip its regular 14-day liquidity operation this week, underlining the change in stance (reuters.com).

Background of Easing Measures

In June, RBI also implemented a 100 bps phased cut in cash reserve ratio (CRR), from 4% to 3% by September, boosting liquidity and improving transmission (fisdom.com, reuters.com).

Market Response

Bond market saw a 6 bps decline in the 10-year yield to ~6.25%. However, short-term yields in the 10–15 bps range may rise (moneycontrol.com).

Strategic Implications

Analysts view the move as RBI’s effort to bring operative rates in line with policy rates, enhancing monetary signal clarity (reuters.com).

Signal of Policy Transition

This marks a shift from easing to fine-tuning liquidity to ensure rate transmission and control inflation (bloomberg.com).

Potential for Further Operations

RBI may conduct more reverse repos if surplus persists, maintaining short-term rate discipline (moneycontrol.com).

Interpretation

The RBI is tightening operational liquidity, a tactical pivot from its earlier accommodative measures.

This move seeks to stabilize the overnight and short-term yield curve, improve policy transmission, and reaffirm the central bank’s credibility.

Investors can expect higher short-term rates, while medium- and long-term yields may remain anchored.

Banks will have less excess cash, potentially leading to tighter credit supply unless RBI offsets via CRR cuts.

The RBI’s move to drain excess liquidity through a ₹1 trillion reverse repo auction has several implications for gilt funds, especially short-duration and long-duration government bond ETFs. Here’s a detailed breakdown:

Implications for Gilt Funds

1. Short-Term Gilt Funds:

Likely Yield Increase: As RBI sucks out liquidity, short-term money market rates (1 day to 1 year) may rise slightly.

NAV Pressure (Mild): Bond prices move inversely to yields. Short-term gilt fund NAVs may see minor declines due to rising short-term yields.

Higher Reinvestment Yield: New money entering these funds may benefit from better accrual rates, improving future returns.

Example Impact: Funds like GILT5YBEES (5-year maturity profile) may experience small fluctuations if short-end yield curve steepens.

2. Long-Term Gilt Funds:

Less Direct Impact: Long-dated government bonds (10–30 years) are less sensitive to temporary liquidity actions unless inflation or repo expectations shift.

Stable or Bullish Bias: If RBI’s liquidity control is seen as anti-inflationary, long-term yields might stay steady or soften, supporting long-duration gilt NAVs.

Example: ETFs like LTGILTBEES (long-term gilt ETF) may remain stable or even benefit slightly.

3. Yield Curve Steepening Possible:

The overnight-to-5-year yields may rise, while the 10–30-year segment remains unchanged.

This steepening curve hurts short-duration gilts more than long ones.

4. Market Sentiment Shift:

The shift from “liquidity infusion” to “drainage” tells markets the RBI is cautious of excess liquidity leading to inflation.

This might prompt investors to move to ultra-short or longer-dated gilts selectively based on their rate view.